18th Aug 2021. 7.47am

Regency View:

Morning Report – Wednesday 18th August

FTSE to open at 7,189 (+9 pts)

UK inflation fell back to the Bank of England’s 2% target – reducing the probability that monetary policy will be tightened…

This morning’s Consumer Price Index (YoY) came in at 2% below forecasts (2.2%) in July with the clothing, recreation and culture sectors dragging the rate of price growth lower.

In Asia it’s been a quiet session with the Hang Seng Index treading water after yesterday’s sell-off.

| S&P 500 | -0.71% | Bearish for UK stocks |

| Hang Seng | +0.66% | Bullish for UK stocks |

| Gold | -0.07% | Neutral for UK stocks |

| AUD/JPY | +0.22% | Neutral for UK stocks |

| US 10yr Yield | -0.09% | Neutral for UK stocks |

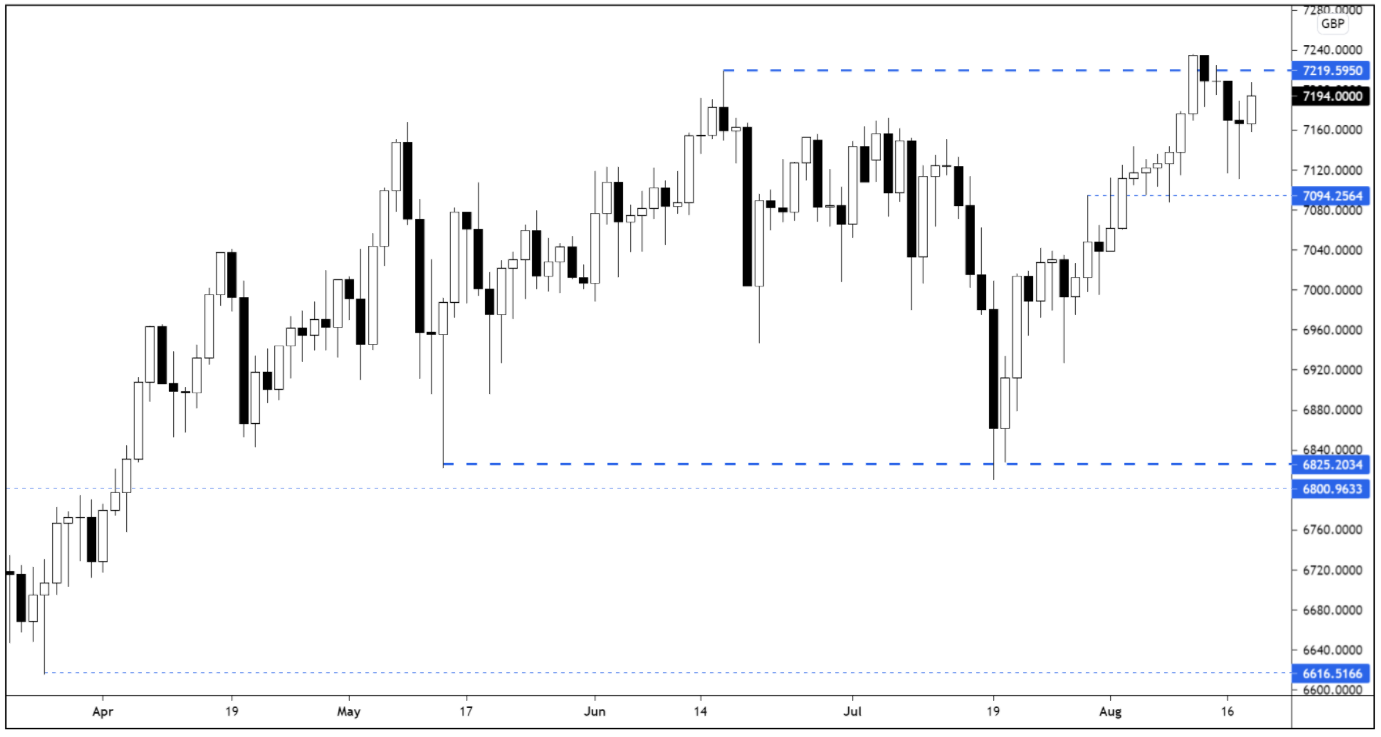

We highlighted in yesterday’s FTSE 100 Technical Outlook video that ‘should the market continue from bullish long-tailed candles then a retest of resistance is likely’ and this has played out within the last 24hrs…

The market closed well above intra-day lows yesterday, and the futures have pushed higher in early trading to take the market back to the key resistance created by the June swing highs – the bulls will be hoping its second time lucky!

FTSE 100 Daily Rolling Futures – Key Levels

| Interim Results |

| Balfour Beatty (BBY) |

| Persimmon (PSN) |

| TBC Bank Group (TBCG) |

| UK Economic Announcements |

| (07:00) Consumer Price Index |

| (07:00) Retail Price Index |

| (07:00) Producer Price Index |

| International Economic Announcements |

| (10:00) Consumer Price Index (EU) |

| (12:00) MBA Mortgage Applications (US) |

| (13:30) Housing Starts (US) |

| (13:30) Building Permits (US) |

| (15:30) Crude Oil Inventories (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.