10th Aug 2022. 7.48am

Regency View:

Morning Report – Wednesday 10th August

FTSE to open at 7,474 (-14 pts)

Stocks on Wall Street continued to tread water near recent highs as investors await today’s key inflation data…

US consumer price index inflation reached 9.1% in June, the highest level in 40 years, which the Fed has met with back-to-back interest rate increases of 0.75 percentage points.

Overnight in Asia, stocks in Hong Kong have sank more than -2% lower – taking the Hang Seng index back to its May lows.

| S&P 500 | -0.42% | Bearish for UK stocks |

| Hang Seng | -2.53% | Bearish for UK stocks |

| Gold | -0.34% | Bullish for UK stocks |

| AUD/JPY | -0.19% | Neutral for UK stocks |

| US 10yr Yield | +22pts | Neutral for UK stocks |

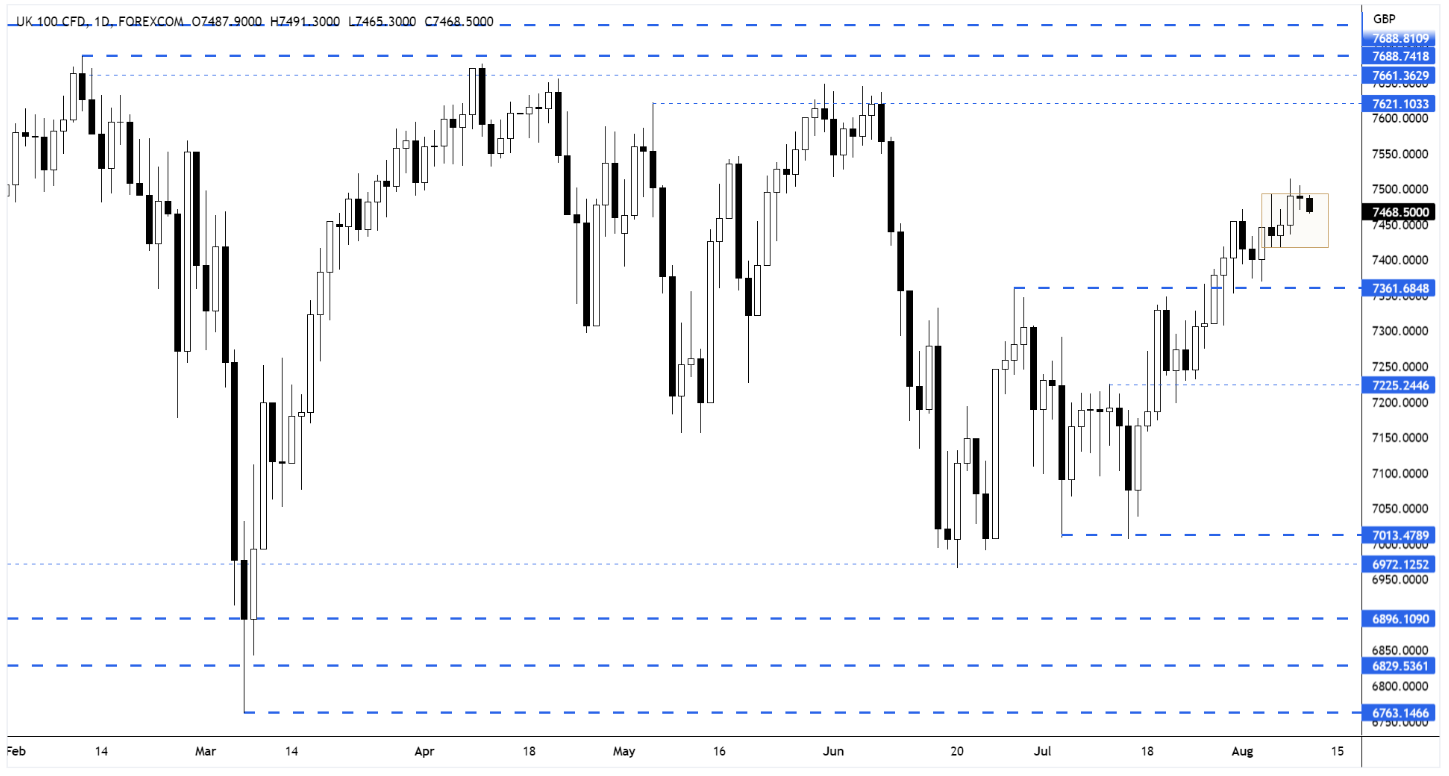

The FTSE daily rolling futures printed its smallest daily range of the year as the market coiled beneath the inside day highs.

This tiny daily range indicates that the market could be set for a multi-day directional move.

FTSE 100 Daily Rolling Futures – Key Levels

| Interim Results |

| ContourGlobal (GLO) |

| Legal & General (LGEN) |

| CLS Holdings (CLI) |

| Genuit Grp Plc (GEN) |

| Hostelworld (HSW) |

| Atalaya Mining (ATYM) |

| Arix Bioscience (ARIX) |

| International Economic Announcements |

| (07:00) Consumer Price Index (GER) |

| (12:00) MBA Mortgage Applications (US) |

| (13:30) Consumer Price Index (US) |

| (15:00) Wholesales Inventories (US) |

| (15:30) Crude Oil Inventories (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.