10th Mar 2022. 7.44am

Regency View:

Morning Report – Thursday 10th March

FTSE to open at 7,163 (-28 pts)

Stocks on Wall Street rallied yesterday as some commodity prices eased…

Brent crude dropped more than 12% yesterday as the market weighed whether major producers would boost supply to help plug the gap in output from Russia.

Asian stocks have tracked the gains on Wall Street, Chinese blue chips jumped 1.73% and Japan’s Nikkei 225 has rallied nearly 4% from its 12-month lows.

Looking ahead today, alongside developments in Ukraine, the market will also be focused on this afternoon’s ECB rate decision and US inflation reading.

| S&P 500 | +2.57% | Bullish for UK stocks |

| Hang Seng | +0.53% | Bullish for UK stocks |

| Gold | -0.59% | Bullish for UK stocks |

| AUD/JPY | +0.40% | Bullish for UK stocks |

| US 10yr Yield | +75pts | Bearish for UK stocks |

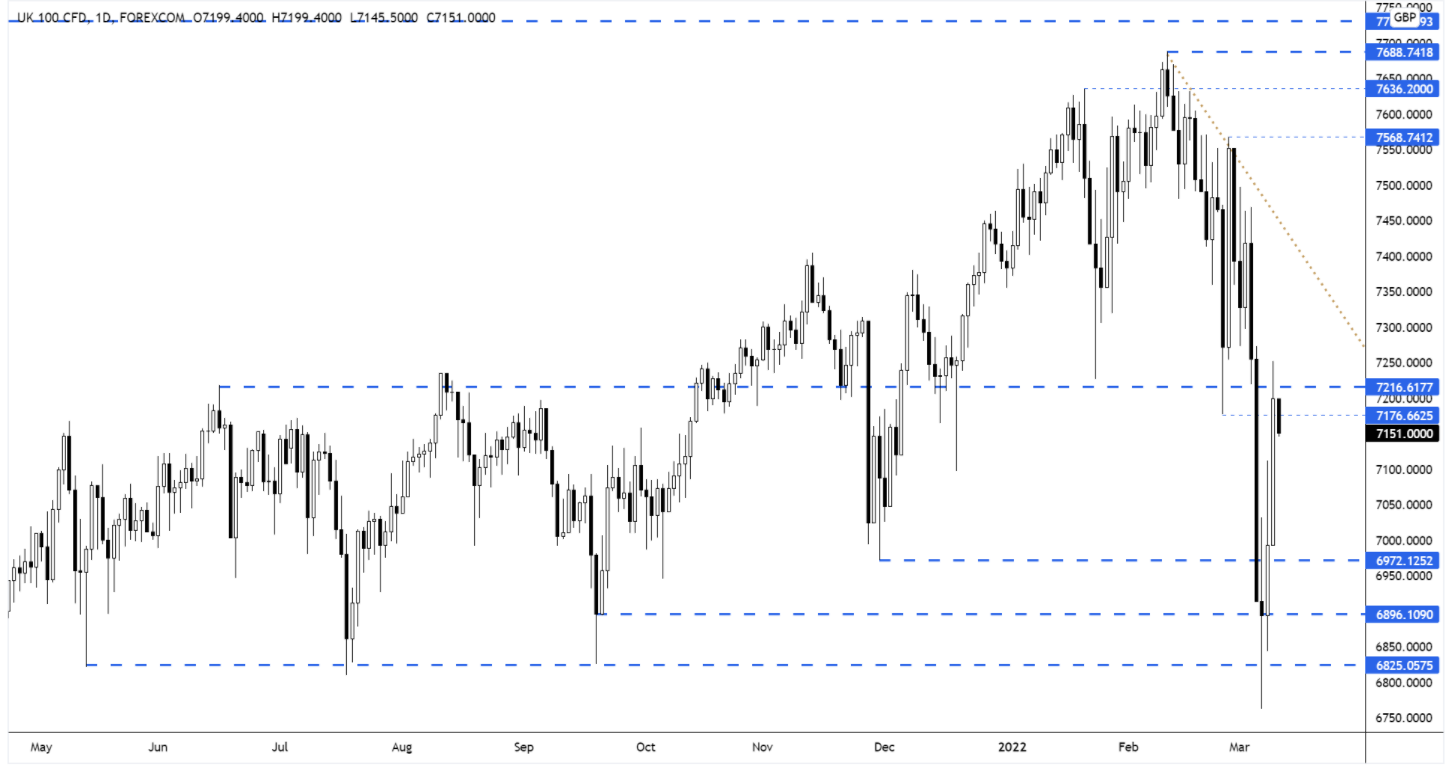

The FTSE’s rally from support continued to gather momentum yesterday – taking prices back to the broken support area at 7,200.

We’ll be watching closely to see if broken support at 7,200 will become resistance, or whether the market can push higher towards the descending trendline.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Hill & Smith (HILS) |

| Spirax-Sarco (SPX) |

| Balfour Beatty (BBY) |

| National Express (NEX) |

| Spirent (SPT) |

| Just Group (JUST) |

| Savills (SVS) |

| Secure Income Reit (SIR) |

| Oakley (OCI) |

| Interim Results |

| Brooks (BRK) |

| Volution Group PLS (FAN) |

| UK Economic Announcements |

| (00:01) RICS Housing Market Survey |

| (07:00) Industrial Production |

| (07:00) Manufacturing Production |

| (07:00) Balance of Trade |

| (07:00) Gross Domestic Product |

| (07:00) Index of Services |

| International Economic Announcements |

| (12:45) ECB Interest Rate (EU) |

| (13:30) Continuing Claims (US) |

| (13:30) Initial Jobless Claims (US) |

| (13:30) Consumer Price Index (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.