10th Feb 2022. 7.46am

Regency View:

Morning Report – Thursday 10th February

FTSE to open at 7,640 (-3 pts)

US stocks rallied for the second consecutive day as traders were buoyed by tech earnings and government bond yields dropping back from recent highs.

There is also increased hope that the Russia / Ukraine tensions can be de-escalated following positive talks between French President Emmanuel Macron and Russian President Vladimir Putin earlier this week.

Overnight in Asia, stocks have given up some of their early gains, but both the Hang Seng and Nikkei remain in small positive territory.

| S&P 500 | +1.45% | Bullish for UK stocks |

| Hang Seng | +0.09% | Neutral for UK stocks |

| Gold | +0.12% | Neutral for UK stocks |

| AUD/JPY | +0.14% | Neutral for UK stocks |

| US 10yr Yield | -21pts | Bullish for UK stocks |

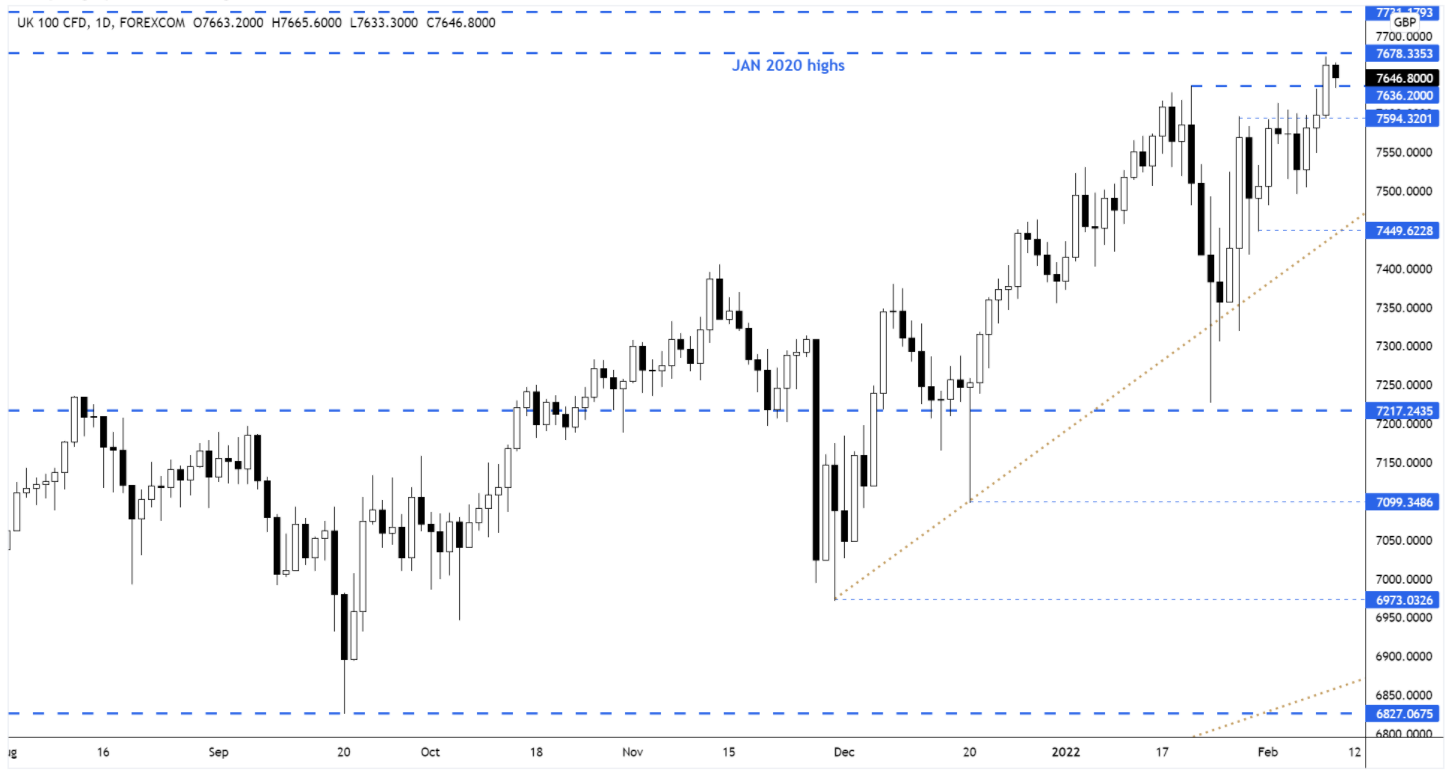

The FTSE burst decisively higher yesterday, taking the market up into those January 2020 pre-pandemic swing highs at 7,678.

We would now expect the broken New Year highs at 7,643 to provide support as the market trends higher.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Astrazeneca (AZN) |

| Relx (REL) |

| Unilever (ULVR) |

| Mmc Norilsk Adr (MNOD) |

| Phosagro S (PHOR) |

| Interim Results |

| Ashmore (ASHM) |

| Redrow (RDW) |

| MJGleeson (GLE) |

| Q4 Results |

| Astrazeneca (AZN) |

| Unilever (ULVR) |

| Trading Announcements |

| Royal Mail (RMG) |

| Watches Switz (WOSG) |

| International Economic Announcements |

| (13:30) Continuing Claims (US) |

| (13:30) Initial Jobless Claims (US) |

| (13:30) Consumer Price Index (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.