28th Mar 2022. 7.43am

Regency View:

Morning Report – Monday 28th March

FTSE to open at 7,500 (+17 pts)

There is increased hopes of progress in Russian-Ukranian peace talks to be held in Turkey this week after President Zelenskiy said Ukraine was prepared to discuss adopting a neutral status as part of a deal.

This news boosted Chinese stocks despite a covid-19 lockdown in Shanghai hitting economic activity, while oil (brent crude) prices dropped $3 per barrel in early trading.

Looking ahead this week, we have a week of consumer price index and producer price index reports from European nations…

There will also be GDP estimates from the US, the UK and Canada, plus international comparisons of business confidence with the manufacturing purchasing managers’ index data on Friday.

| S&P 500 | +0.51% | Bearish for UK stocks |

| Hang Seng | +0.66% | Bullish for UK stocks |

| Gold | -1.10% | Bullish for UK stocks |

| AUD/JPY | +0.92% | Bullish for UK stocks |

| US 10yr Yield | -103pts | Bearish for UK stocks |

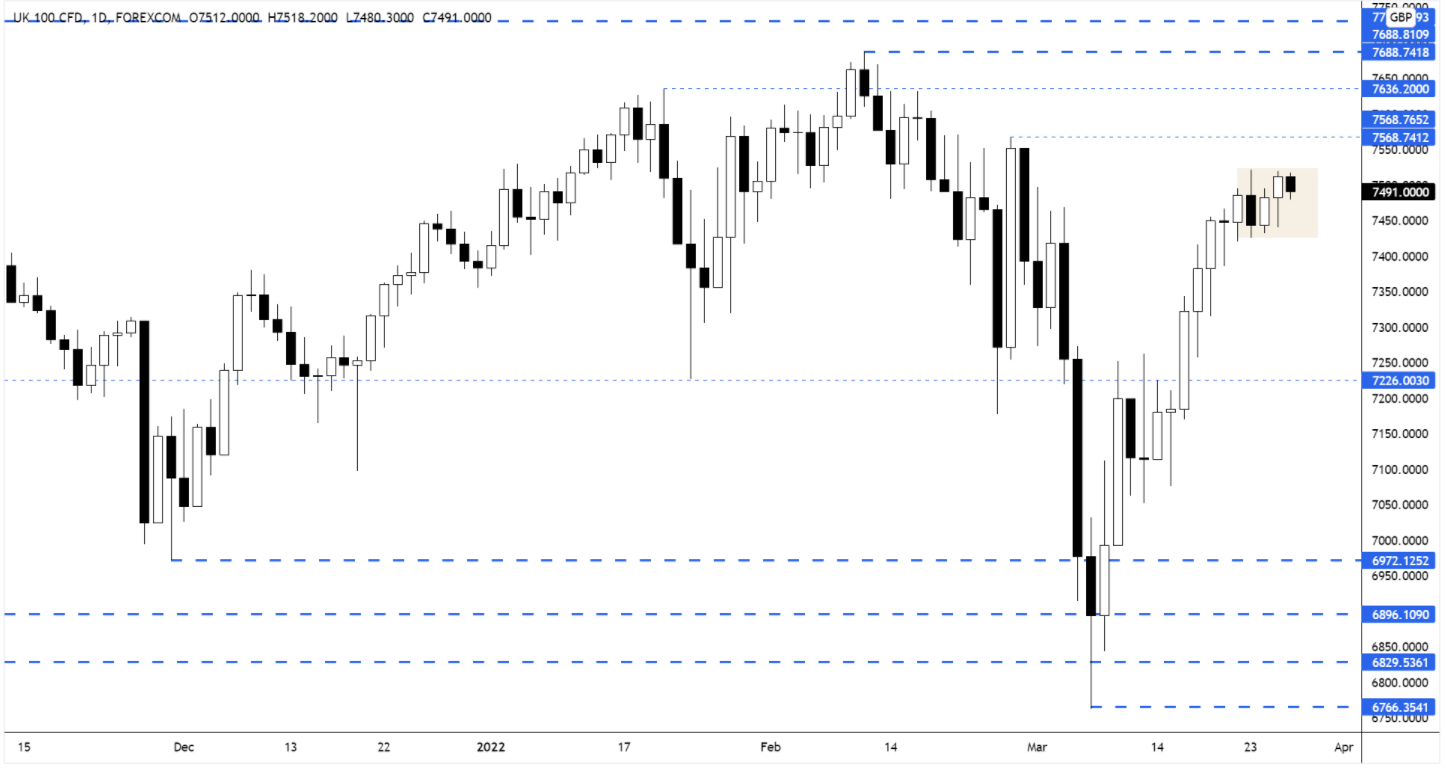

The inside day pattern which formed on Thursday remains very much in play – with Wednesday’s range key to our short-term directional bias.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Dialight (DIA) |

| Tandem Group (TND) |

| Rtc Grp. (RTC) |

| Globaltrans (GLTR) |

| Octopus Renew (ORIT) |

| UK Economic Announcements |

| (11:00) BoE’s Governor Bailey speech |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.