25th Apr 2022. 7.46am

Regency View:

Morning Report – Monday 25th April

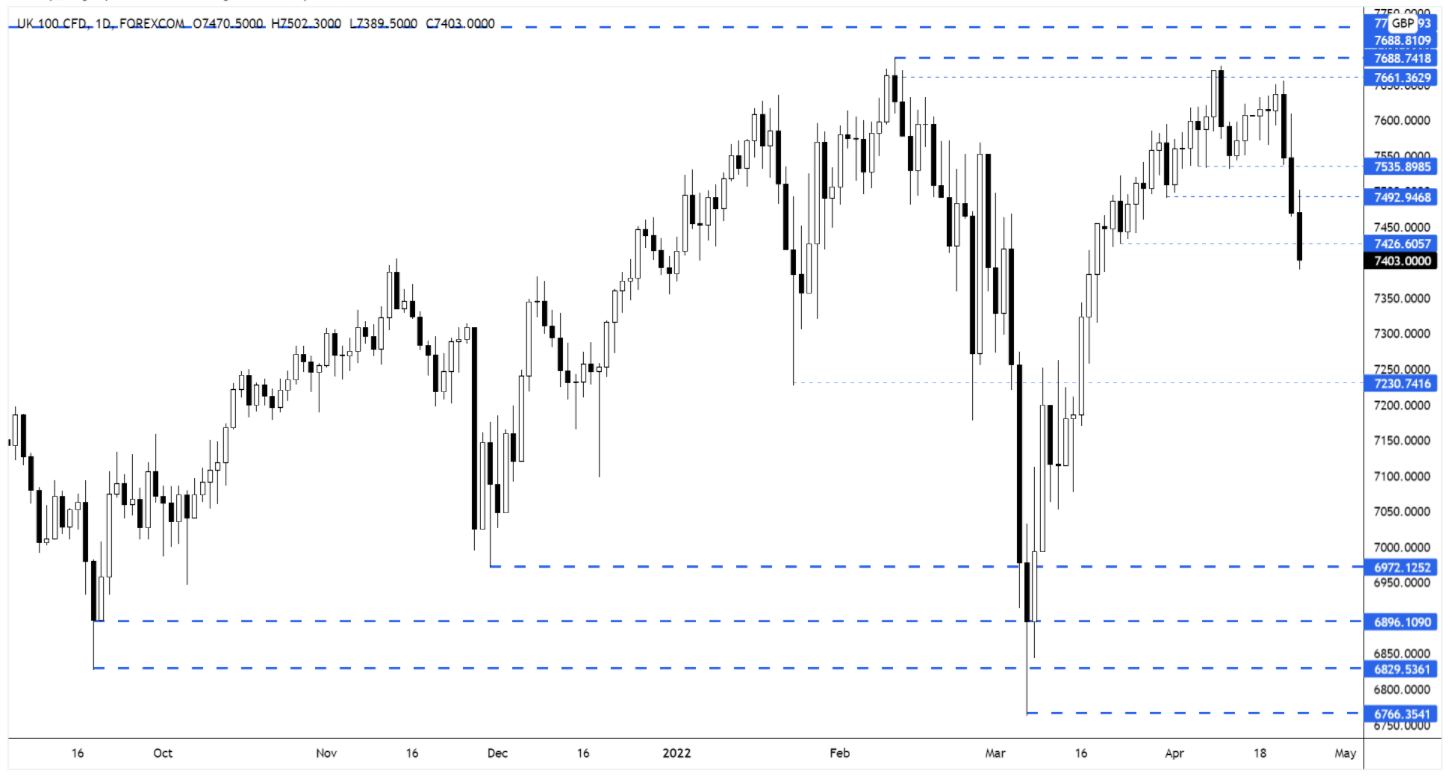

FTSE to open at 7,403 (-119 pts)

French incumbent president Emmanuel Macron is to be re-elected for a second term after defeating his far-right rival Marine Le Pen in Sunday’s run-off – the markets ‘priced-in’ this win on Friday with the euro rallying 95pts against the pound.

While Asian trading has seen stocks mirror Friday’s heavy losses on Wall Street, caused by the anticipation of aggressive monetary tightening from the Fed.

Looking ahead this week, we have another raft of inflation numbers, this time from eurozone countries. We also have GDP estimates from the US, Korea, Germany and eurozone, along with an interest rate decision from the Bank of Japan.

| S&P 500 | -2.77% | Bearish for UK stocks |

| Hang Seng | -3.50% | Bearish for UK stocks |

| Gold | -0.90% | Bullish for UK stocks |

| AUD/JPY | -1.97% | Bearish for UK stocks |

| US 10yr Yield | -10pts | Neutral for UK stocks |

Friday’s price action saw the FTSE fail to hold onto its early gains and selling pressure accelerated into the closing bell – causing the index the slice through multiple levels of support.

The selling pressure have continued during the early hours, and the cash market is set to open below support (see chart).

Short-term momentum now firmly favours the bears.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Frenkel Topping (FEN) |

| Audioboom Grp. (BOOM) |

| Arecor Therape (AREC) |

| International Economic Announcements |

| (15:00) BoC’s Governor Macklem speech (CAD) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.