1st Nov 2021. 7.45am

Regency View:

Morning Report – Monday 1st November

FTSE to open at 7,268 (+30 pts)

It’s been a mixed Asian session with Chinese-focused stocks falling for a fifth straight session. Whereas Japan’s Nikkei 225 jumped to a 1-month high after Prime Minister Fumio Kishida’s Liberal Democratic Party did better than expected at Sunday’s election.

Looking ahead this week, the market’s focus will be on tightening monetary policy…

On Wednesday, the US Federal Reserve is widely expected to announce that it will start reducing its pandemic-era bond purchases. While on Thursday, the Bank of England is expected to hike interest rates to combat inflationary pressures.

| S&P 500 | +0.19% | Neutral for UK stocks |

| Hang Seng | -0.97% | Bearish for UK stocks |

| Gold | +0.08% | Neutral for UK stocks |

| AUD/JPY | -0.02% | Neutral for UK stocks |

| US 10yr Yield | -1.15% | Bullish for UK stocks |

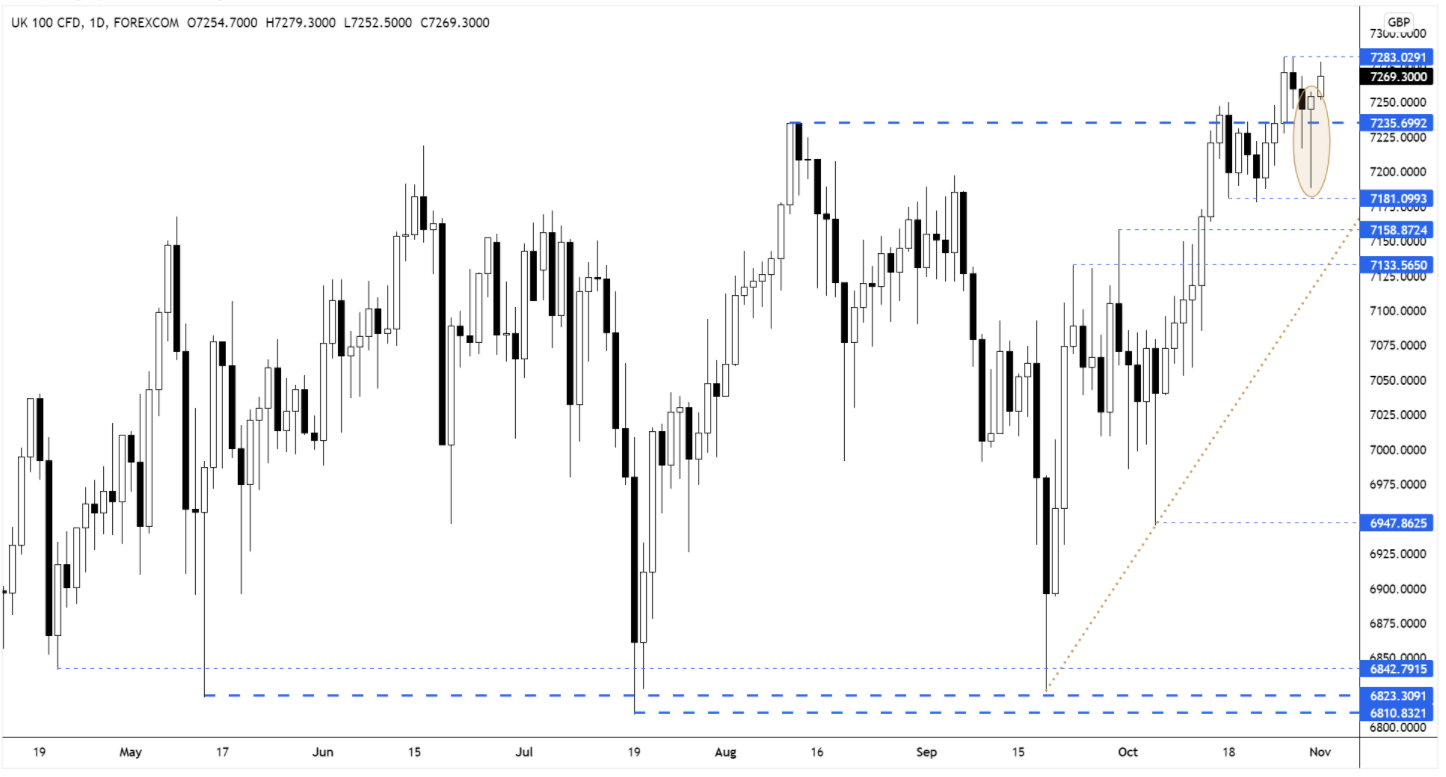

Friday’s price action saw the FTSE fight all the way back from it’s intra-day lows to close back above resistance and form its second consecutive bullish pin-bar candle.

A break and hold above last week’s highs could finally trigger the trend continuation move higher that last week’s break and retest of resistance signaled.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| K3 Capital Gro. (K3C) |

| Lok N Store (LOK) |

| Trading Announcements |

| Argo Blockchai. (ARB) |

| UK Economic Announcements |

| (09:30) PMI Manufacturing |

| International Economic Announcements |

| (07:00) Retail Sales (GER) |

| (08:55) PMI Manufacturing (GER) |

| (14:45) PMI Manufacturing (US) |

| (15:00) Construction Spending (US) |

| (20:30) Auto Sales (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.