26th Aug 2022. 7.37am

Regency View:

Morning Report – Friday 26th August

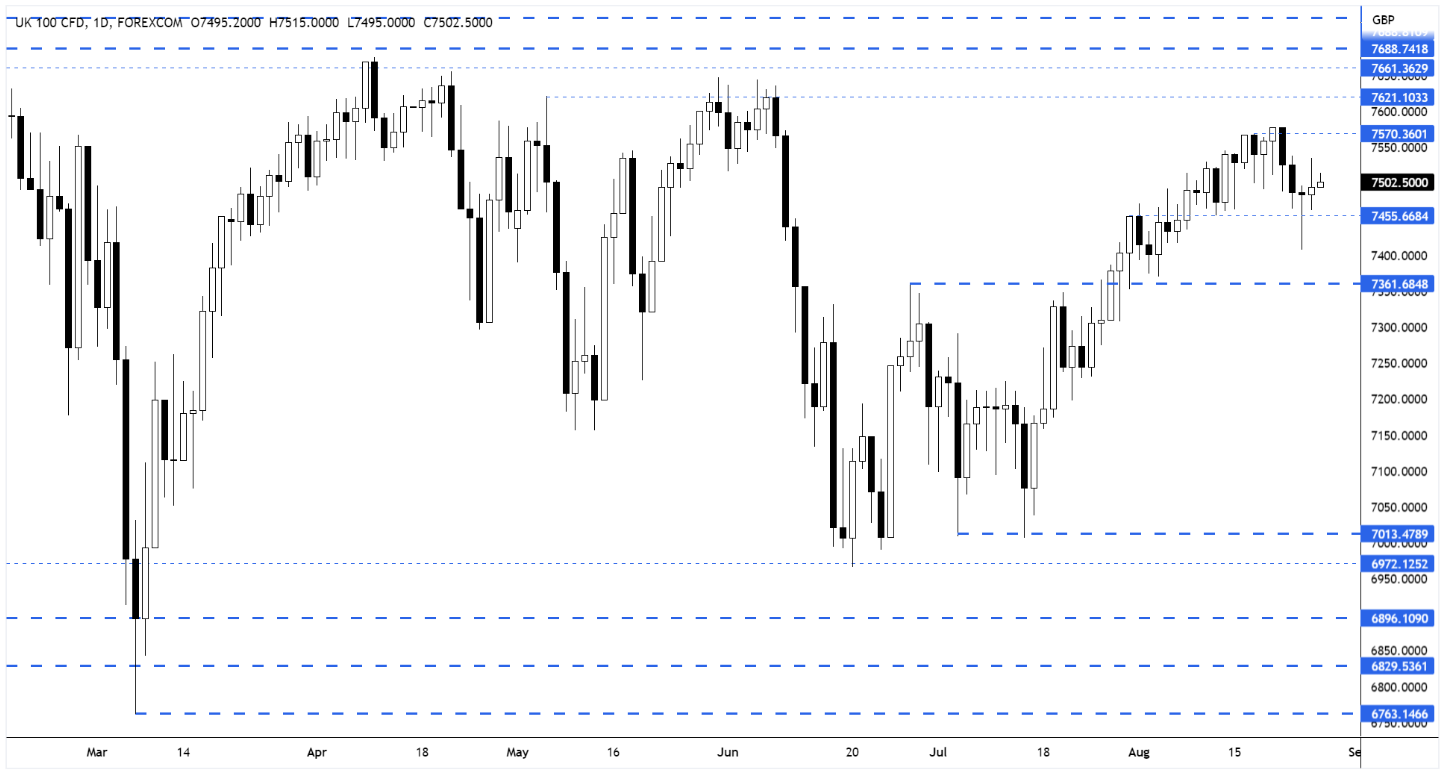

FTSE to open at 7,507 (+27 pts)

Stocks on Wall Street rallied yesterday as the US economy shrank less than previously reported in the second quarter and the labour market remained in robust shape…

The second estimate of US GDP was revised down to a contraction of 0.6% from its first estimate of a 0.9% decline – economists had predicted a decrease of 0.8%.

Overnight in Asia, stocks have followed Wall Street higher amid signs that the US and China are close to resolving a longstanding impasse over audits of Chinese companies.

| S&P 500 | +1.41% | Bullish for UK stocks |

| Hang Seng | +0.67% | Bullish for UK stocks |

| Gold | -0.01% | Neutral for UK stocks |

| AUD/JPY | +0.10% | Neutral for UK stocks |

| US 10yr Yield | -79pts | Bullish for UK stocks |

Yesterday’s price action saw the FTSE initially rally from the bullish pin-bar which formed on Wednesday, only to give back more than half its gains during afternoon trading.

This indecisive price action is indicative is to be somewhat expected ahead of tomorrow’s speech from Fed Chair Jerome Powell at the Jackson Hole Symposium.

FTSE 100 Daily Rolling Futures – Key Levels

| International Economic Announcements |

| (07:00) GFK Consumer Confidence (GER) |

| (09:00) M3 Money Supply (EU) |

| (13:30) Personal Consumption Expenditures (US) |

| (13:30) Personal Income (US) |

| (13:30) Personal Spending (US) |

| (13:30) Balance of Trade (US) |

| (14:00) Fed’s Chair Powell speech (US) |

| (14:00) Jackson Hole Symposium (US) |

| (15:00) U. of Michigan Confidence (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.