25th Jun 2021. 7.34am

Regency View:

Morning Report – Friday 25th June

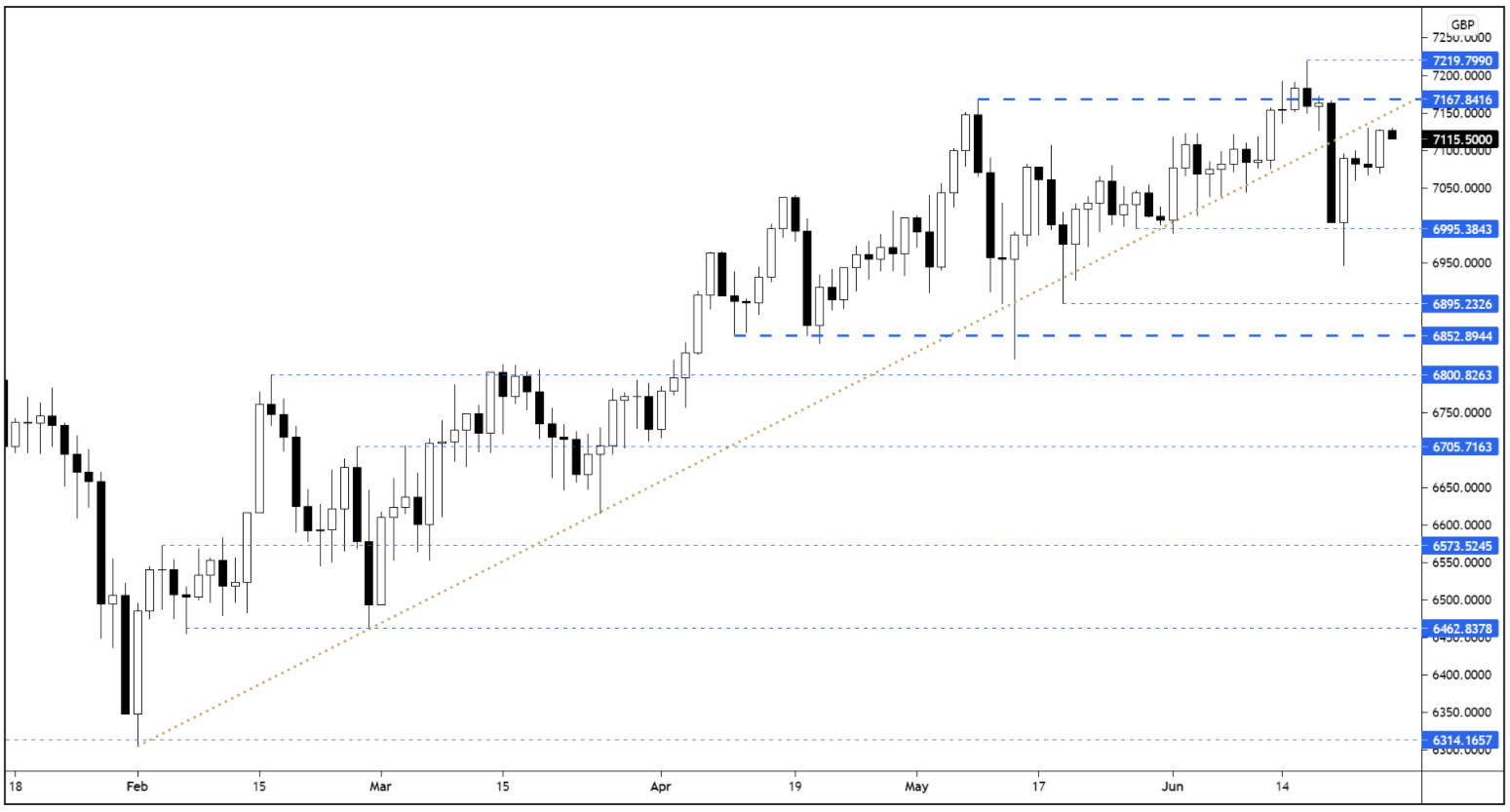

FTSE to open at 7,117 (+7 pts)

Stocks on Wall Street posted another record close yesterday as President Joe Biden gained bipartisan backing for a revised infrastructure deal worth $1tn.

The revised deal is smaller than the original $2.3tn deal proposed in March, but it provides markets with much needed clarity over US government spending plans.

Asian stocks have been lifted by the US market and our Risk Barometer has a bullish feel to it as we head into the European open.

| S&P 500 | +1.58% | Bullish for UK stocks |

| Hang Seng | +1.38% | Bullish for UK stocks |

| Gold | +0.22% | Neutral for UK stocks |

| AUD/JPY | +0.16% | Neutral for UK stocks |

| US 10yr Yield | +0.58% | Neutral for UK stocks |

The FTSE rallied up into Wednesday’s highs during yesterday’s session – putting in a strong close. However, the market is now faced with multiple layers of short-term resistance which will likely see some profit taking as we head into the weekend.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Jade Road Inv (JADE) |

| Norman Broadb (NBB) |

| UK Economic Announcements |

| (00:01) GFK Consumer Confidence |

| International Economic Announcements |

| (07:00) GFK Consumer Confidence (GER) |

| (09:00) M3 Money Supply (EU) |

| (13:30) Personal Consumption Expenditures (US) |

| (13:30) Personal Income (US) |

| (13:30) Personal Spending (US) |

| (15:00) U. of Michigan Confidence (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.