3rd Jun 2021. 7.45am

Regency View:

Morning Report – Thursday 3rd June

FTSE to open at 7,100 (-8 pts)

It was a quiet session on both sides of the Atlantic yesterday, as traders sit on their hands ahead of Friday’s key non-farm payrolls number.

The tug of war between the strong growth ‘reopening trade’ versus the fear that inflation will be more than transitory, has seen markets flip flop for the last month or two and it is hoped that Friday’s non-farm’s should provide some clarity.

In Asia, Hong Kong’s Hang Seng is set for its weakest session in nearly a month while Japan’s Nikkei 225 is up on optimism over the countries vaccine roll-out.

| S&P 500 | +0.14% | Neutral for UK stocks |

| Hang Seng | -0.82% | Bearish for UK stocks |

| Gold | -0.51% | Bullish for UK stocks |

| AUD/JPY | -0.04% | Neutral for UK stocks |

| US 10yr Yield | -1.66% | Bullish for UK stocks |

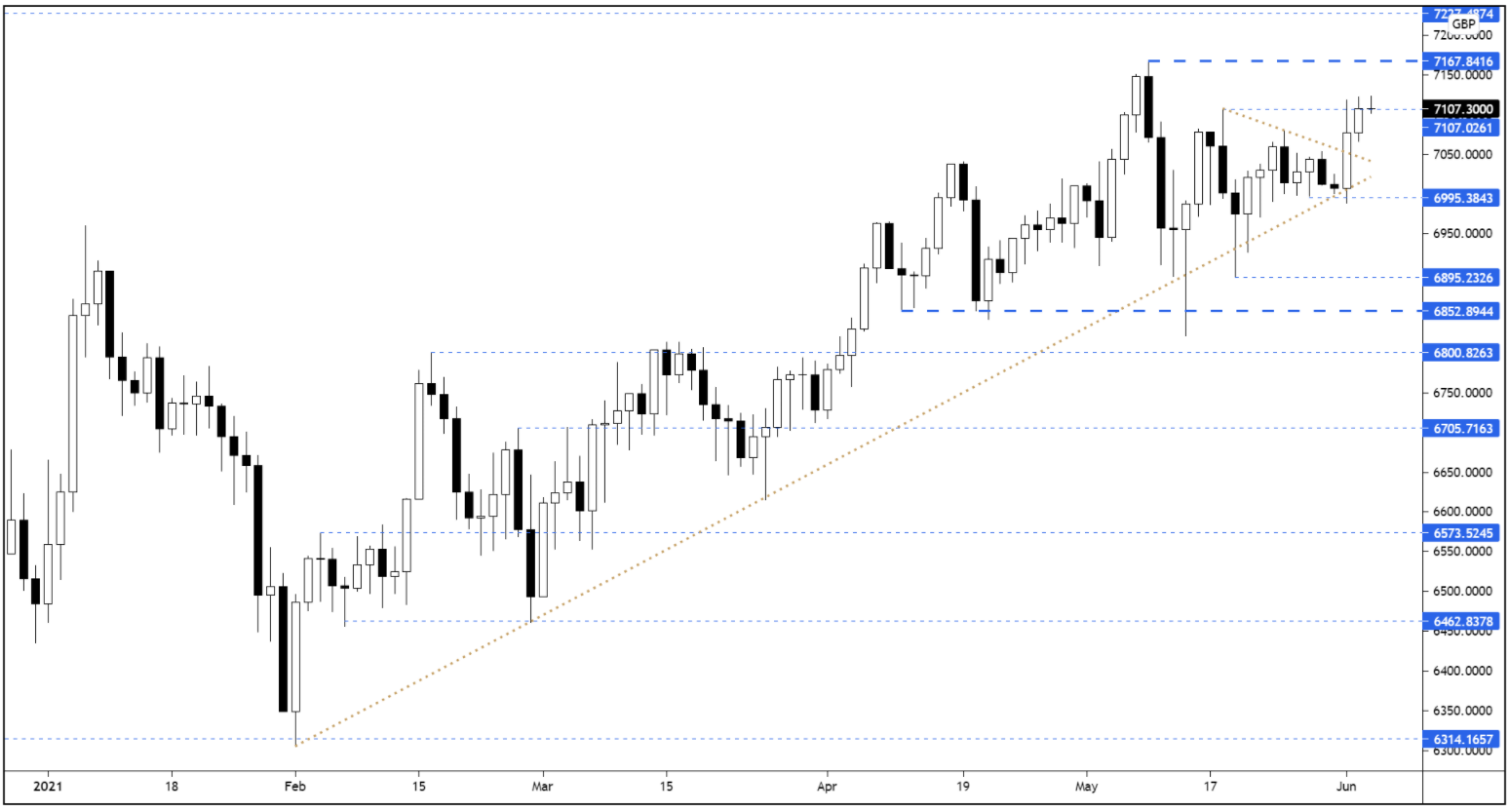

The FTSE had a steady session yesterday, consolidating Tuesday’s breakout gains…

With the cash market set to open right on the short-term resistance level at 7,107, price action during the opening rotation will be well worth a watch.

Despite the short-term resistance, probabilities favour a retest of the May swing highs at 7,167.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Braemar Shipping (BMS) |

| Discoverie Grp. (DSCV) |

| NewRiver (NRR) |

| Pennon (PNN) |

| Workspace (WKP) |

| UK Economic Announcements |

| (09:30) PMI Services |

| International Economic Announcements |

| (08:55) PMI Services (GER) |

| (08:55) PMI Composite (GER) |

| (09:00) PMI Composite (EU) |

| (09:00) PMI Services (EU) |

| (13:30) Continuing Claims (US) |

| (13:30) Initial Jobless Claims (US) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.