28th Jun 2022. 7.47am

Regency View:

Morning Report – Tuesday 28th June

FTSE to open at 7,317 (+59 pts)

Wall Street’s recovery ran out of steam yesterday with the S&P 500 edging lower after strong gains on Friday.

Oil prices have pushed higher despite G7 members exploring ways of curbing energy costs, including possible caps on the price of oil and gas.

Overnight in Asia, the Hang Seng is set for its fourth consecutive session of gains after China’s central bank governor pledged to maintain an accommodative monetary stance and stressed that its inflationary outlook was “stable”.

| S&P 500 | -0.30% | Bearish for UK stocks |

| Hang Seng | +0.62% | Bullish for UK stocks |

| Gold | +0.30% | Bearish for UK stocks |

| AUD/JPY | +0.57% | Bullish for UK stocks |

| US 10yr Yield | +74pts | Bearish for UK stocks |

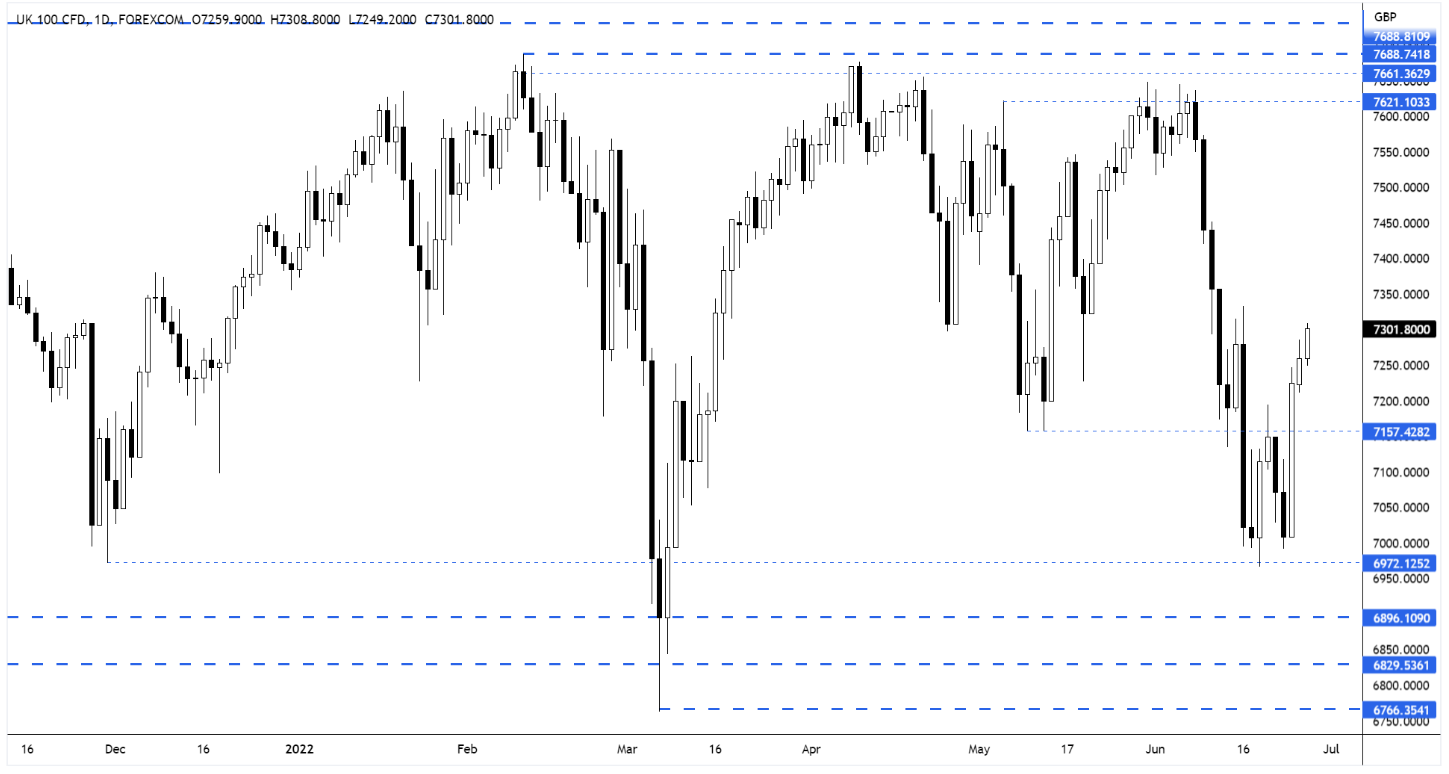

As mentioned in yesterday’s Morning Report, Friday’s strong, counter-momentum rally could setup a more substantial rally back towards the 7,400 mid-range area.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Wise Plc (WISE) |

| International Economic Announcements |

| (08:00) ECB’s President Lagarde speech |

| (13:00) US Housing Price Index (MoM)(Apr) |

| (13:00) S&P/Case-Shiller Home Price Indices (YoY)(Apr) |

| (14:00) US Consumer Confidence (Jun) |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.