22nd Mar 2022. 7.42am

Regency View:

Morning Report – Tuesday 22nd March

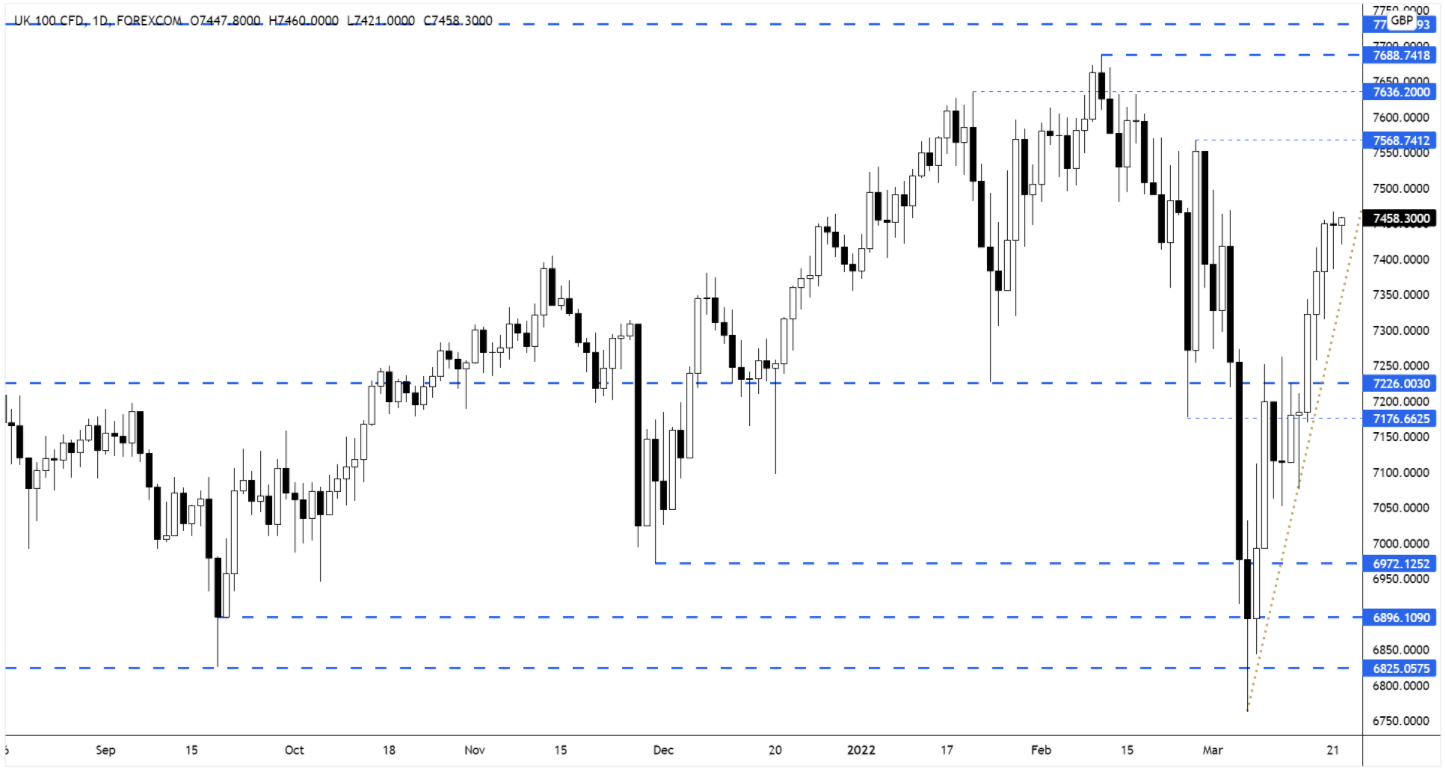

FTSE to open at 7,455 (+13 pts)

The yield on US 10yr Treasury’s surged 145 points yesterday as high inflation pushes the Fed to aggressively pull back monetary stimulus…

The rise in bond yields (fall in prices) marks the worst month for US Treasury’s since Donald Trump was elected president in 2016.

While overnight in Asia, gains in banks, energy and mining stocks lifted Hong Kong’s Hang Seng and Japan’s Nikkei 225 index rallying more than +1.50%.

| S&P 500 | -0.04% | Neutral for UK stocks |

| Hang Seng | +2.99% | Bullish for UK stocks |

| Gold | -0.11% | Neutral for UK stocks |

| AUD/JPY | +0.67% | Bullish for UK stocks |

| US 10yr Yield | +145pts | Bearish for UK stocks |

Yesterday’s price action saw the FTSE quickly bounce from its opening lows to close flat on the day…

This reluctance to pullback should be viewed as a bullish sign. However, we may see yesterday’s highs provide some short-term resistance.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Alliance Pharma (APH) |

| The Pebble Gro. (PEBB) |

| Diaceutics (DXRX) |

| Kape Tech. (KAPE) |

| Staffline (STAF) |

| Fintel (FNTL) |

| Sabre Insur (SBRE) |

| Oxford Nano (ONT) |

| Luceco (LUCE) |

| Zotefoams (ZTF) |

| Longboat Energy (LBE) |

| Yu Group (YU.) |

| Interim Results |

| YouGov (YOU) |

| Scs Group (SCS) |

| Softcat (SCT) |

| Diurnal Grp (DNL) |

| International Economic Announcements |

| (13:15) ECB’s President Lagarde speech |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.