16th Feb 2022. 7.44am

Regency View:

Morning Report – Wednesday 16th February

FTSE to open at 7,604 (-5 pts)

Wall Street rallied for the first time in three sessions yesterday as after Russia said it had begun pulling some troops back to their bases. Brent crude also pulled back from trend highs as tensions eased.

Overnight in Asia, stocks have mirrored the rally on Wall Street with the Hang Seng and Nikkei firmly in positive territory.

While this morning’s UK inflation data saw consumer prices rise at annual rate of 5.5%, more than analysts expected and its fastest pace since 1992.

Looking ahead this afternoon we have US retail sales and FOMC minutes, which are sure to get the market’s attention given the current inflationary environment.

| S&P 500 | +1.58% | Bullish for UK stocks |

| Hang Seng | +1.30% | Bullish for UK stocks |

| Gold | +0.10% | Neutral for UK stocks |

| AUD/JPY | +0.38% | Bullish for UK stocks |

| US 10yr Yield | +60pts | Bearish for UK stocks |

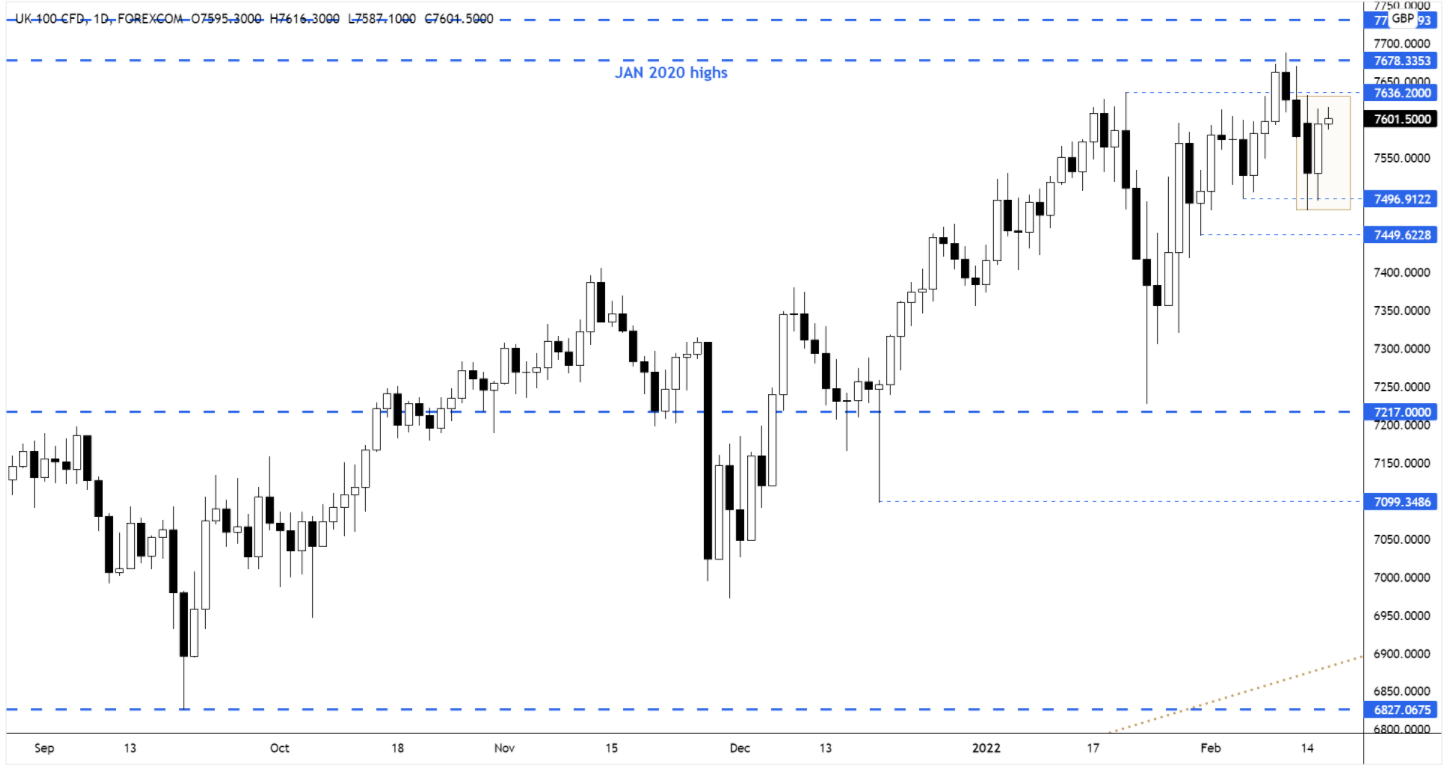

Yesterday’s price action on the FTSE saw the market bounce from support, but remain within Monday’s range – forming an ‘inside day’ pattern.

The parameters of the inside day (Monday’s range) become significant with a break above / below being a signal of directional bias.

FTSE 100 Daily Rolling Futures – Key Levels

| Final Results |

| Segro (SGRO) |

| Primary Health (PHP) |

| Indivior (INDV) |

| Kerry (KYGA) |

| Interim Results |

| BHP Group (BHP) |

| UK Economic Announcements |

| (07:00) Retail Price Index |

| (07:00) Consumer Price Index |

| (07:00) Producer Price Index |

| International Economic Announcements |

| (13:30) Retail Sales (MoM) (Jan) |

| (19:00) FOMC Minutes |

Don’t have a Regency account yet?

Start receiving our actionable Market Alerts and Analysis with real-time email and SMS alerts throughout your trading day. Simply click below to create your account for free.

Create AccountAny Questions? Please feel free to call 0203 973 8007 or email us at info@regency.capital

Disclaimer:

This research is prepared for general information only and should not be construed as any form of investment advice.